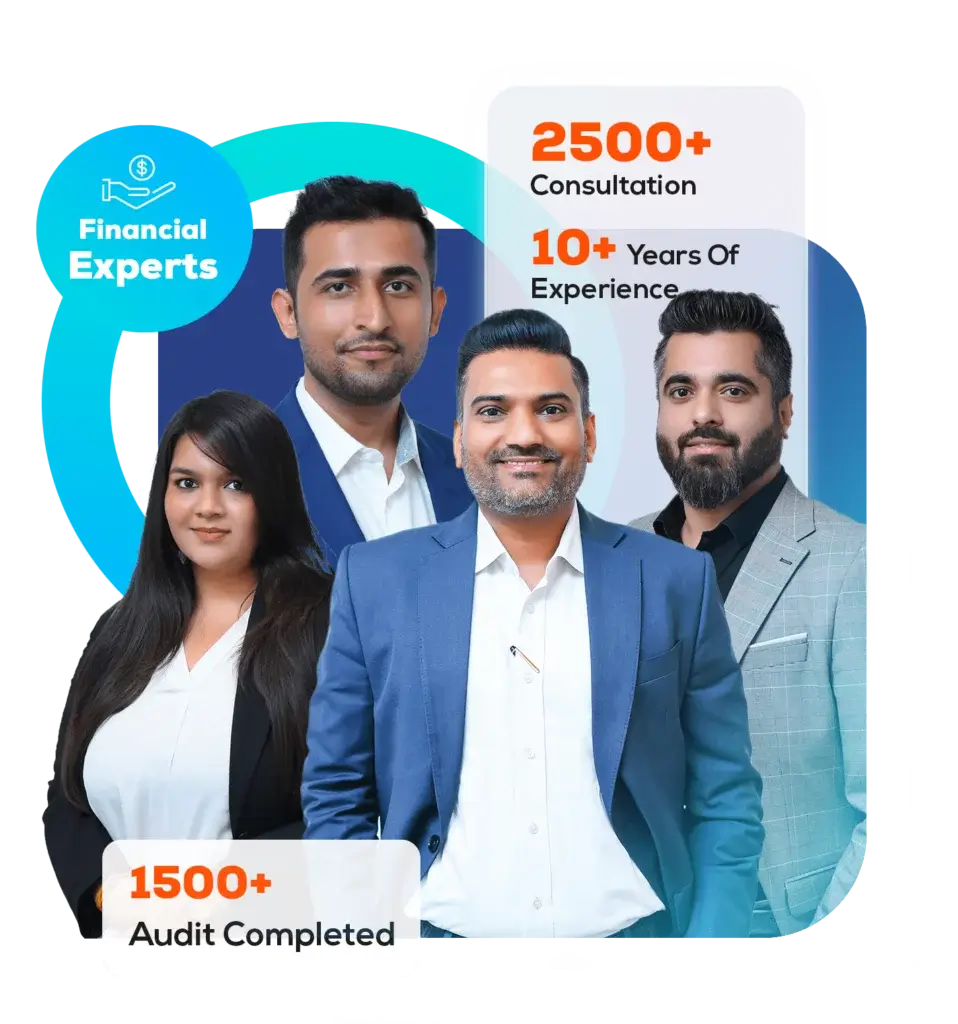

Audit Completed

Experts

Expert Guidance for Budgeting

Audits provide detailed information and help you identify costs and their allocations. Based on the data, an auditor would guide you to make informed decisions about cost allocations for various tasks in the future.

Compliance Assurance

By engaging professional CPAs and auditors, you enable your business to remain compliant with local and international regulations. Auditing determines whether the financial statements comply with the UAE’s financial standards. If errors are found, you can rectify them immediately.

Fraud and Error Detection

Professional auditing services in Dubai review your business’s financial records and history. This provides credible data related to all the transactions made in a specific time period. By careful analysis, you can find errors that can result in loss for your business and also identify fraudulent activities, if any.

-

Expertise

Our team of auditing experts can help you breeze through the complexities of audit processes. Reach out to us for all your auditing needs in Dubai.

-

Ease

We intend to guide clients from A to Z with our exclusive and comprehensive audit services for Dubai-based companies.

-

Clarity

At Avyanco, we start each audit process by gaining a complete understanding of our clients, their business processes, and their specific requirements.

Ravi

Mansur

Himanshu